Three years ago we had $847 in our checking account on the day before payday. Rent was $1,200. I sat at my kitchen table at 11pm doing math that didn’t work no matter how many times I redid it. We were two adults with decent jobs and we couldn’t cover our basic bills without juggling due dates and hoping nothing unexpected happened.

- The Brutal Truth About Our Spending

- Change #1: The One Week Spending Freeze

- Change #2: The Four Wall Budget

- Change #3: The Cash Envelope System For Groceries

- Change #4: The Subscription Audit

- Change #5: Meal Planning To Reduce Food Waste

- Change #6: The 24-Hour Rule For Non-Essential Purchases

- Change #7: Switching To Generic Brands

- Change #8: The Side Hustle That Actually Helped

- Change #9: The Debt Snowball Method

- Change #10: Building A Tiny Emergency Fund

- Change #11: Asking For Help When We Needed It

- Change #12: Celebrating Small Wins

- What’s Different Now

- The Tools That Helped

- What I’d Tell Someone Starting This Journey

- The Real Goal

That was our rock bottom moment. The moment I realized living paycheck to paycheck wasn’t just temporary bad luck or poor planning. We were stuck in a cycle and if we didn’t change something, we’d be stuck forever.

I’m not going to tell you we fixed everything overnight with one weird trick. We didn’t. It took almost two years to get to a place where we had consistent money left at the end of the month. But these 12 changes are what got us there.

The Brutal Truth About Our Spending

The first thing I had to do was track every single dollar we spent for one month. Not to judge it, not to change it yet, just to see where the money was actually going. Because I genuinely didn’t know.

I thought we were spending our money on bills and groceries and necessities. Turns out we were spending way more than I realized on stuff I didn’t even remember buying. $8 here for fast food breakfast because we were running late. $15 there for random Target purchases. $40 for a subscription service I forgot we had.

None of those purchases felt significant in the moment. But when I added them up for the month, we’d spent almost $600 on what I’d categorize as “I don’t even know.” Not planned purchases, not things we needed, just random spending that happened because we weren’t paying attention.

That was painful to see. But I needed to see it because I couldn’t fix what I didn’t know was broken.

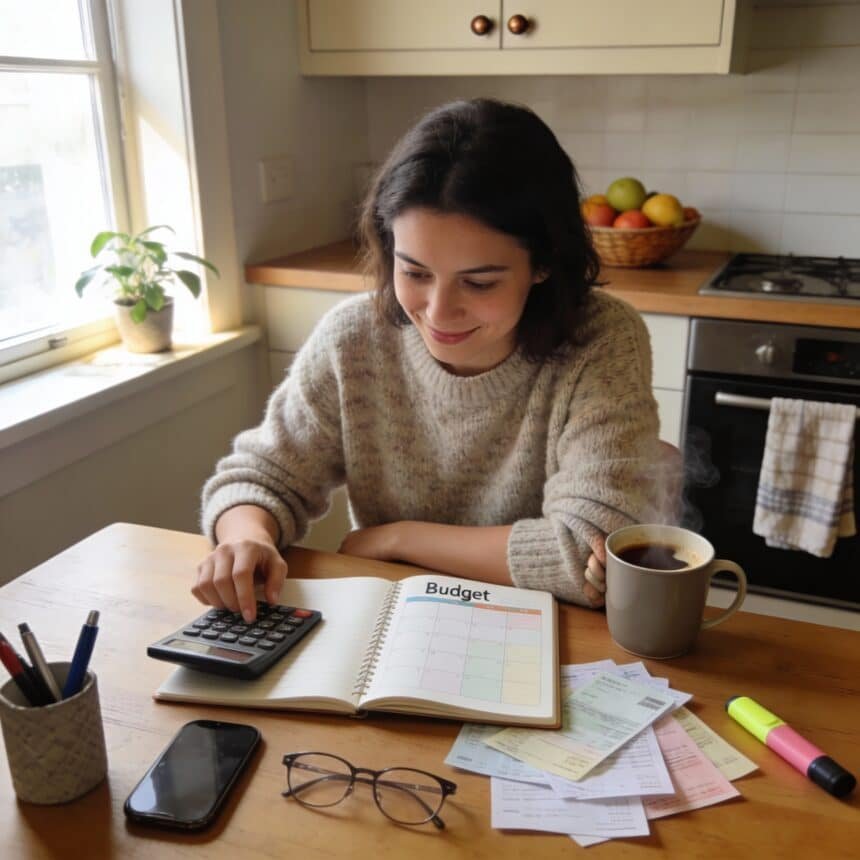

I used a simple budget planner notebook to track everything. Not an app, not a spreadsheet, an actual physical notebook. For me personally, writing things down by hand made it more real. I couldn’t ignore it.

Change #1: The One Week Spending Freeze

Once I knew where our money was going, I needed to stop the bleeding. So we did a one-week spending freeze. We bought nothing except absolute necessities for seven days. No eating out, no online shopping, no random purchases.

We used what we had in the pantry and freezer for meals. We stayed home instead of going out. We said no to everything.

It was hard. Not because we were deprived, but because I realized how much of our spending was just habit. We’d stop for coffee because that’s what we did in the morning. We’d order pizza on Friday because that’s what we always did. Breaking those patterns even for a week was uncomfortable.

But we saved $200 that week. Two hundred dollars that normally would have just evaporated. That proved to me that we did have money, we were just spending it unconsciously.

Change #2: The Four Wall Budget

I learned about this concept from Dave Ramsey and it changed how I thought about budgeting. The four walls are food, shelter, utilities, and transportation. Everything else comes after those are covered.

I made a list of our true necessities and their actual costs. Rent, electricity, water, gas for the cars, minimum payments on debt, groceries. That was it. Everything else was negotiable.

This gave me a baseline. If we could cover the four walls, we’d survive. Everything else was bonus. This took so much pressure off because I stopped trying to fund everything at once and started prioritizing ruthlessly.

When money was tight, the four walls got paid first. Period. No exceptions. Everything else could wait.

Change #3: The Cash Envelope System For Groceries

We were overspending on groceries constantly. I’d go to the store intending to spend $100 and walk out having spent $150. Every single time.

So I switched to cash for groceries. I took out $400 at the beginning of the month and divided it into four envelopes, one for each week. When the cash was gone, we were done shopping for the week.

This forced me to meal plan because I couldn’t just buy whatever looked good. I had to think about what we actually needed and stick to the list. It also made me much more aware of prices. When you’re watching physical cash leave your hand, you think harder about whether you really need that thing.

You can use a cash envelope system for this or just regular envelopes from your desk. The point is the cash, not the fancy envelopes.

We cut our grocery spending by almost $200 a month just by switching to cash. Same family, same food needs, but way more intentional spending.

Change #4: The Subscription Audit

I went through our bank statements and wrote down every single recurring charge. Subscriptions, memberships, automatic payments, all of it. Then I cancelled everything we weren’t actively using.

We had a gym membership we hadn’t used in four months. A streaming service we’d signed up for one show and forgotten to cancel. A monthly subscription box that was fine but not necessary. Magazine subscriptions. App subscriptions. It was ridiculous.

I cancelled nine things in one afternoon and freed up $127 per month. That’s over $1,500 a year we were just throwing away on stuff we didn’t use or didn’t need.

The subscriptions that were worth keeping, I kept. But I was way more conscious about them after that. Every few months I do another audit to make sure we’re not paying for things we’re not using.

Change #5: Meal Planning To Reduce Food Waste

We were wasting so much food. I’d buy groceries with vague intentions of cooking, then we’d be tired and order takeout, and the groceries would go bad. We were literally throwing money in the trash.

I started meal planning every single week. On Sunday I’d sit down and plan out dinners for the next seven days. Then I’d make a grocery list based on those meals and buy only what was on the list.

This did two things. First, it eliminated food waste because we were buying ingredients for specific meals we were actually going to cook. Second, it eliminated the temptation to order takeout because we had a plan and ingredients already at home.

If you need help with the meal planning process, check out the meal planning system that saved our grocery budget. It walks through exactly how to plan meals efficiently.

We went from throwing away probably $75 worth of food every month to almost zero food waste. That’s $75 that stayed in our account instead of going in the garbage.

Change #6: The 24-Hour Rule For Non-Essential Purchases

Anytime I wanted to buy something that wasn’t on my list or in my budget, I had to wait 24 hours before buying it. No impulse purchases allowed.

This was hard at first. When I saw something I wanted, my brain would come up with all these justifications for why I needed it right now. But forcing myself to wait almost always resulted in not buying it.

After 24 hours, the impulse would fade. I’d realize I didn’t actually want the thing that much, or I’d remember I already had something similar at home, or I’d decide the money was better spent elsewhere.

This probably saved us $200 to $300 a month just by eliminating impulse buying. Not because we never bought anything, but because we were way more intentional about what we chose to buy.

Change #7: Switching To Generic Brands

I had this weird brand loyalty thing where I thought name brand was always better quality. Turns out for most products, generic is exactly the same.

I started buying store brand everything. Groceries, cleaning supplies, toiletries, all of it. And honestly? I couldn’t tell the difference for 90% of items.

The few things where the name brand actually was better, I kept buying name brand. But for most stuff, generic worked just fine and cost 30 to 50% less.

This saved us probably $50 to $80 a month on groceries and household items. It doesn’t sound like much but when you’re living paycheck to paycheck, $80 matters.

Change #8: The Side Hustle That Actually Helped

I know everyone says to get a side hustle, and honestly that advice always felt insulting to me. Like I wasn’t already working hard enough? But once I got our spending under control, I realized we needed to also increase income if we were going to get ahead.

I didn’t do anything fancy. I started doing online surveys during my lunch break and while watching TV at night. I also picked up occasional freelance writing gigs when I had time. Neither was consistent big money, but together they brought in an extra $200 to $400 a month.

That money went straight to paying down debt, which eventually freed up more monthly cash flow. It wasn’t glamorous and it wasn’t fun, but it helped.

The key was finding side income that fit into my existing schedule without making me more exhausted. I couldn’t take on a second job with set hours because of the kids. But flexible stuff I could do from home? That worked.

Change #9: The Debt Snowball Method

We had credit card debt, car payments, and student loans. The minimum payments were killing us. I couldn’t see a way out.

Then I learned about the debt snowball method. You list all your debts smallest to largest, make minimum payments on everything, and throw any extra money at the smallest debt until it’s gone. Then you roll that payment into the next smallest debt.

I know mathematically it makes more sense to pay off highest interest first. But psychologically, I needed wins. Paying off that first small credit card gave me momentum. It proved we could do this.

We paid off three small debts in the first eight months. Each time we paid one off, we had a little more monthly cash flow. That extra breathing room made everything less stressful.

Change #10: Building A Tiny Emergency Fund

When you’re paycheck to paycheck, the idea of an emergency fund feels impossible. How can you save money when there’s nothing left to save?

But I started with $20 a month. That’s it. Twenty dollars that I’d take out as cash and put in an envelope before I paid bills. Some months I could only do $10. A couple months I couldn’t do anything. But I kept trying.

After a year, I had $180 saved. That doesn’t sound like much, but it meant when my car needed a small repair, I had cash to cover it instead of putting it on a credit card. That was huge.

Once I got to $500 saved, so many small emergencies stopped being emergencies. The stress relief of knowing I had something to fall back on was incredible.

If you can’t save $20 a month, save $5. Save something. Even if it’s just change from cash purchases. Start somewhere.

Change #11: Asking For Help When We Needed It

This was the hardest one for me. I didn’t want to admit we were struggling. I didn’t want to ask for help. I felt like we should be able to handle this ourselves.

But when we were really in trouble, I called our utility company and asked about payment plans. I called our landlord and asked if we could pay rent in two installments that month instead of all at once. I asked family if they could watch the kids instead of paying for childcare for a few months.

Everyone said yes. The utility company had programs I didn’t know existed. Our landlord worked with us. Family was happy to help.

Nobody judged us. Nobody made us feel bad. They just helped.

If you’re struggling, ask. Ask creditors about hardship programs. Ask utility companies about payment plans. Ask family and friends for specific help with specific things. You might be surprised by how many people are willing to work with you.

Change #12: Celebrating Small Wins

When you’re in survival mode financially, it’s easy to focus on how far you still have to go. How much debt you still have. How far away your goals are.

I had to intentionally celebrate small wins or I’d have given up. Paid off a small debt? We celebrated. Stayed under budget for a month? We celebrated. Built the emergency fund to $100? We celebrated.

The celebrations were free or cheap. Homemade special dinner, movie night at home, playing a game as a family. Just something to acknowledge progress.

This kept me going. It reminded me that we were moving forward even when it felt slow. It gave me hope that things could actually change.

What’s Different Now

We’re not rich. We’re not even particularly comfortable financially. But we’re not living paycheck to paycheck anymore. We have a small emergency fund. We’re paying down debt. We can handle small unexpected expenses without panicking.

That peace of mind is worth more than I can explain. I don’t lie awake at night doing math anymore. I don’t avoid checking my bank account because I’m scared of what I’ll see. I don’t feel that constant background stress about money.

It took two years to get here. Two years of being intentional about every dollar. Two years of saying no to things we wanted. Two years of slow progress that sometimes felt like no progress.

But it worked. Not perfectly, not easily, but it worked.

The Tools That Helped

I mentioned the budget planner notebook and cash envelopes already. The other tool that really helped was a simple calculator that I kept in my kitchen. Not my phone calculator, an actual calculator that lived on my counter.

Having it visible and accessible meant I’d actually use it to check math before making purchases or paying bills. I’d add up what I was about to buy at the grocery store before I got to checkout. I’d calculate what I could afford to put toward debt this month. I’d figure out if we could afford something before saying yes to it.

This sounds basic but it made a difference. When the calculator was in front of me, I did the math. When I had to dig out my phone, I’d skip the math and just hope it worked out. Hope is not a financial strategy.

What I’d Tell Someone Starting This Journey

Start with tracking your spending for one month. Don’t change anything yet, just see where the money goes. You can’t fix what you don’t measure.

Then pick one change from this list. Just one. Do that for a month until it feels automatic. Then add another change.

Don’t try to fix everything at once. That’s overwhelming and you’ll burn out and quit. Small consistent changes compound over time.

Be patient with yourself. You’re not going to solve years of financial stress in three weeks. This is a slow process. That’s okay. Slow progress is still progress.

And please, don’t beat yourself up. You’re trying. You’re learning. You’re making changes. That’s what matters.

If you need help with the practical side of setting up a budget and getting organized, check out the beginner’s guide to budgeting when you hate budgeting. It’s way less intimidating than most budget advice.

The Real Goal

The goal isn’t to be perfect with money. The goal isn’t to never spend on anything fun or never make mistakes. The goal is just to get out of survival mode.

To have enough breathing room that a flat tire doesn’t become a crisis. To be able to cover your bills without juggling due dates. To sleep at night without worrying about money.

That’s what these changes gave us. Not wealth, not luxury, just stability. And honestly? After living paycheck to paycheck for so long, stability feels like winning.

If you’re in that paycheck to paycheck cycle right now, you can break it. It won’t be fast and it won’t be easy, but you can do it. One change at a time, one month at a time, one small win at a time.

Amazon Disclosure:

As an Amazon Associate, I earn from qualifying purchases. This means if you click on an Amazon link and make a purchase, I may receive a small commission at no extra cost to you. I only recommend products I actually use and believe will help you.

{kind=link}

What change made the biggest impact for your family budget? Share your tips and don’t forget to check out the post! #FamilyFinances #Budgeting #CozyCornerDaily