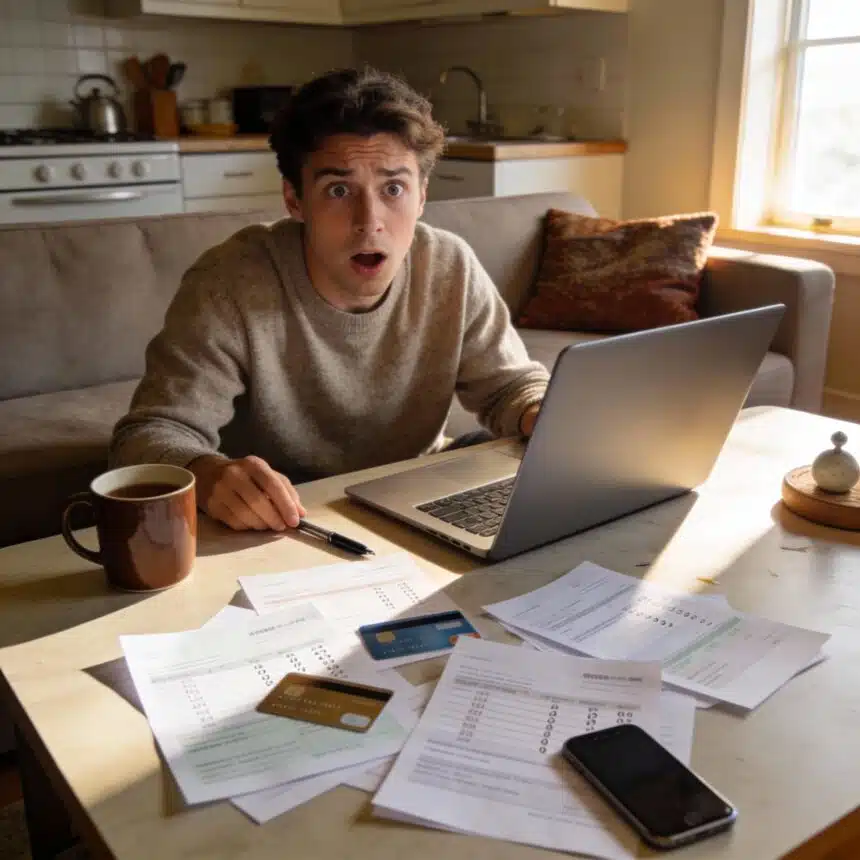

I was reviewing our credit card statement in January trying to figure out where all our money was going and I kept seeing these charges I didn’t recognize. $6.99 here, $12.99 there, a bunch of $9.99 charges for different things.

- How I Had No Idea This Was Happening

- The Full List Of What I Was Paying For

- How I Tracked Them All Down

- The Ones That Were Genuinely Hard To Cancel

- What I Kept And Why

- The Budget Impact Was Immediate

- The Quarterly Audit I Do Now

- What Other People Found When They Did This

- The Free Trial Trap

- Teaching My Kids About Subscription Costs

- The Mental Load Of Managing This

- The Spending Pattern I Noticed

- What I’d Tell Someone Else Doing This

- The Long Term Strategy

At first I thought maybe my card got stolen. But then I started googling the company names and realized they were all subscriptions. Streaming services, app subscriptions, memberships, things I’d signed up for months or even years ago and completely forgotten about.

When I added them all up, we were paying $127 every single month for stuff we weren’t using. Some of them I didn’t even remember signing up for in the first place. That’s over $1,500 a year. Just gone. For nothing.

This is apparently super common now. There’s even a name for it, subscription creep. The average person is paying for way more subscriptions than they think they have, and a bunch of them are things they don’t use or don’t even know about anymore.

I spent one afternoon going through everything and canceling what we didn’t need. Got $127 a month back in our budget. Here’s how I did it and what I found.

How I Had No Idea This Was Happening

The thing about subscriptions is they’re designed to be invisible. Small charges spread across different cards and different months. You sign up for a free trial, forget to cancel, and suddenly you’re paying for something you used once.

Or you sign up for something you genuinely wanted at the time, use it for a while, stop using it, but never actually cancel. The charge keeps happening automatically every month and you just don’t notice because it’s mixed in with all your other spending.

Some companies make canceling deliberately hard too. You have to call during business hours, or navigate through five pages of “are you sure?” prompts, or remember a password you set up two years ago. So even when you think about canceling, it’s enough friction that you put it off and forget again.

That’s what happened to us. I meant to cancel a meal kit service months ago but it required calling during their phone hours which I kept forgetting to do. So we just kept getting charged $89 every two weeks for meal kits we weren’t ordering.

The Full List Of What I Was Paying For

When I finally sat down and went through everything, here’s what I found. This is embarrassing but I’m sharing it because I bet other people have similar situations and just don’t know it yet.

Netflix, which we use all the time, fine that one stays. Hulu with ads, also use it, keep. But then there was Disney Plus that we got during COVID to keep the kids entertained and literally haven’t opened in six months. $7.99 a month for nothing.

HBO Max that I signed up for to watch one show, watched the show, never cancelled. $15.99 a month.

A meditation app I used twice. $12.99 a month.

A language learning app I was excited about for approximately one week. $9.99 a month.

Amazon Music Unlimited on top of Prime, which I didn’t even realize was a separate charge. $9.99 a month.

A recipe app with meal planning features. $6.99 a month. I used it maybe three times total.

That meal kit service I mentioned, $89 every two weeks, which is basically $178 a month.

A news subscription I signed up for during the election and forgot existed. $9.99 a month.

Cloud storage I apparently upgraded at some point and never downgraded back. Extra $4.99 a month.

A fitness app I used during my short-lived workout phase last spring. $14.99 a month.

And gym membership I straight up forgot we had because it’s been charging a card I barely use. $35 a month for a gym I haven’t been to since before my second kid was born.

That’s $127 a month. Some months it was even higher if the meal kit charged twice in one month.

How I Tracked Them All Down

I started by going through three months of credit card statements on both cards we use regularly. I highlighted every recurring charge I saw. Anything that showed up every month or every couple weeks.

Then I made a list of all those companies and googled each one because some of them I genuinely didn’t recognize the company name. Turns out some subscriptions charge under their parent company name which is different from the app or service name you actually signed up for.

Once I had the full list, I went through and marked which ones we actually use and which ones we don’t. I was honest with myself. If we haven’t used it in the last month, we’re not using it. I wasn’t keeping things we “might” use someday.

The meal kit service was the biggest one and the hardest to track down because they charge every other week, not monthly, so it took me a while to notice the pattern. And they charge under a slightly different name than their main brand.

I also checked my email for subscription confirmation emails. Search for “subscription” and “billing” in your email and you’ll find a bunch of stuff. Some companies email you monthly statements even if you ignore them, which helped me find a couple I’d missed on the credit card statements.

The Ones That Were Genuinely Hard To Cancel

Most of them I could cancel online in like two minutes. Go to account settings, find “cancel subscription,” click a few buttons, done. But a few companies make it deliberately difficult.

The meal kit service required me to call them during specific hours. I had to call twice because the first time I was on hold for 20 minutes and then my kid started screaming and I had to hang up. The second time I got through and they tried really hard to convince me not to cancel. Offered me discounts, tried to switch me to a different plan, the whole thing. I just kept saying no thank you I want to cancel.

The gym membership was a nightmare. I had to go in person with my ID to cancel. You can sign up online but you can’t cancel online. So I had to drive there, find time during their weekday hours, and fill out a form. Took 45 minutes out of my day just to stop giving them money.

The news subscription required me to log in, but I couldn’t remember my password and the password reset wasn’t working. I ended up having to email customer service and wait three days for them to manually cancel it on their end.

If a company is making it hard to cancel, that’s a red flag. They’re banking on you giving up. Don’t give up. Just keep pushing through the friction until it’s cancelled. It’s your money.

What I Kept And Why

I didn’t cancel everything. We kept Netflix and Hulu because we genuinely use them multiple times a week and they’re how we unwind after the kids go to bed. That’s worth the cost to us.

We kept Amazon Prime because we use the free shipping constantly and the video is a bonus. That one pays for itself in shipping costs alone.

I kept Spotify family plan because we all use it every day. My kids listen to music while playing, I listen while cleaning, my husband listens during his commute. That’s genuine value for our family.

The key was being honest about what we actually use versus what we think we should use or might use someday. If we’re not using it right now, consistently, we don’t need to be paying for it right now.

If we decide we want Disney Plus again someday, we can resubscribe. It’s not like it goes away forever if you cancel. But paying for it month after month just in case we might watch something eventually is throwing money away.

The Budget Impact Was Immediate

Getting $127 a month back was huge for our budget. That’s real money that we can now use for things that actually matter to us instead of it just disappearing into subscriptions we don’t use.

We put most of it toward paying down debt. Some of it went into our emergency fund which was basically non-existent before. Having that extra breathing room every month changed how stressed I felt about money.

It’s not like canceling subscriptions solved all our financial problems. We were still living pretty tight. But it was one piece of getting control over where our money was actually going instead of just leaking out everywhere.

If you’re trying to get your budget under control too, check out the brutally honest budget that finally worked. Same concept of being really real about where money’s going and plugging the leaks.

The Quarterly Audit I Do Now

I learned my lesson. Now every three months I go through our credit card statements and check for subscriptions again. It’s on my calendar. I spend 20 minutes making sure we’re not paying for anything we don’t need anymore.

This catches things before they become a problem. If we signed up for a free trial and forgot to cancel, I’ll catch it after one or two months instead of a year later. If we subscribed to something and stopped using it, same thing.

It also helps me stay aware of how many subscriptions we have total. It’s easy to think “oh it’s only $9.99” but when you have six things that are “only $9.99” that’s $60 a month.

I keep a running list now of our active subscriptions in a note on my phone. The name, how much it costs, what date it charges. This makes the quarterly audit way faster because I can just compare my list to my credit card statement and see if anything new appeared or if anything on my list isn’t being used anymore.

What Other People Found When They Did This

I posted about this in a budget group online and so many people replied saying they did the same thing and found a bunch of forgotten subscriptions too. One person found $200 a month. Another person found a magazine subscription they’d been paying for for five years and had moved twice so weren’t even receiving the magazines anymore.

Someone else found they were paying for two different cloud storage services because they’d switched services but never cancelled the first one. Another person was paying for a subscription box they’d completely forgotten existed.

The common thread was everyone thought they had a pretty good handle on their subscriptions until they actually went through everything and realized they didn’t. Subscription creep is so common because it’s designed to be invisible.

The Free Trial Trap

A huge part of how I ended up with so many subscriptions was free trials. You sign up to try something, it asks for your credit card “just for verification,” and then after the trial ends it starts charging you automatically.

Most people intend to cancel before the trial ends. But you forget, or you’re busy, or you lose track of when the trial actually ends, and boom you’re subscribed.

Now I don’t sign up for free trials unless I set a reminder on my phone for two days before the trial ends. That gives me time to cancel if I don’t want to keep it. If I can’t be bothered to set the reminder, I probably don’t actually need the thing.

I also take a screenshot of the trial end date and put it in a folder on my phone called “Cancel By.” This has saved me from accidentally subscribing to probably a dozen things over the last year.

Teaching My Kids About Subscription Costs

My kids are getting old enough to start asking for app subscriptions and game passes and all that stuff. So this whole situation became a teaching moment about how subscriptions work and why you have to be careful with them.

We talk about how $9.99 doesn’t sound like much, but if you have five things that cost that, it’s $50 a month. And that’s $600 a year. That’s a lot of money for apps and games.

They don’t get unlimited subscriptions. They each get to pick one thing they really want and we’ll pay for that, but they have to actually be using it. If they stop using it for a month, we cancel it. They can pick something different later if they want.

This is helping them understand that digital stuff costs real money even though it doesn’t feel as “real” as buying something physical. And that subscriptions are an ongoing cost, not a one-time thing.

If you’re trying to teach your kids about money in general, check out how we talk about money in front of our kids. It’s helped make these conversations feel normal instead of awkward.

The Mental Load Of Managing This

One frustrating thing about subscriptions is they add mental load. You have to remember what you’re subscribed to, when things charge, when to cancel trials, all of it. It’s one more thing to track and manage.

Having a system helps. My quarterly audit and my phone note with the list of active subscriptions means I don’t have to actively remember this stuff constantly. I just check in every few months and make sure everything’s still accurate.

But honestly I’d rather have fewer subscriptions just to reduce the mental load. Fewer things to track, fewer charges to watch for, fewer decisions about whether to keep or cancel things. Simpler is better.

This is similar to how I approach our evening routine. The fewer things I have to actively think about and remember, the better. Make systems that work automatically so your brain is free for other stuff.

The Spending Pattern I Noticed

When I looked at when I’d signed up for most of these subscriptions, there was definitely a pattern. I subscribe to stuff when I’m stressed or overwhelmed and looking for a solution.

Stressed about not being in shape? Subscribe to a fitness app. Stressed about not knowing what to make for dinner? Subscribe to a meal kit service. Stressed about not meditating enough? Subscribe to a meditation app.

But subscribing doesn’t actually solve the problem. It just makes me feel like I’m doing something about it for a minute. Then I don’t actually use the thing and I’ve just added another expense.

Realizing this pattern helped me be way more skeptical of my impulse to subscribe to things. Now when I want to sign up for something, I wait a week and see if I still think it’s necessary. Usually I don’t.

If you’re dealing with similar stress spending patterns, check out I stopped the Amazon overspending spiral. Different type of spending but same impulse control stuff.

What I’d Tell Someone Else Doing This

Do the audit. It’s probably going to take an hour or two to go through everything thoroughly, but it’s worth it. You’ll almost definitely find stuff you forgot about.

Be ruthless about what you keep. If you’re not using it right now, cancel it. You can always resubscribe later if you actually miss it. But chances are you won’t even notice it’s gone.

Make canceling easy for yourself. Don’t put it off because it requires a phone call or whatever. Just do it right away while you’re thinking about it. Set aside an afternoon, cancel everything you don’t need, and be done with it.

Set up a system to prevent this from happening again. My quarterly audit works for me. Maybe you need monthly. Maybe you use a subscription tracking app. Whatever works, just have something in place.

And be careful with free trials from now on. They’re designed to convert into paid subscriptions. Only sign up if you actually think you’ll use the thing, and set a reminder to cancel if you don’t want to keep it.

The Long Term Strategy

Getting $127 a month back was great. But the bigger win was changing how I think about subscriptions. Now I’m way more intentional about what I sign up for and way more diligent about canceling things we’re not using.

This is part of the bigger picture of taking control of our finances instead of just letting money flow out automatically and hoping there’s enough left at the end of the month. Every automatic payment is something to evaluate and make an active choice about.

This connects to a lot of the other changes we made when we were living paycheck to paycheck. It’s all about being aware and intentional instead of just reactive.

That $127 a month is still in our budget over a year later. We didn’t let new subscriptions creep back in. We stayed strict about only paying for things we actually use. And it’s made a real difference in how much breathing room we have financially.

If you want a structured plan rather than individual tips, The Family Budget Reset ($22) is a 30-day framework for identifying exactly where the money is going and reassigning it — built specifically for families, not single earners.

For books and tools that go deeper on this topic, Amazon has a solid selection worth browsing.

{kind=link}

Wow, $127 is quite a bit! How much did you guys find when you checked your subscriptions? Don’t forget to read the link for tips! #MoneySaver #Budgeting #CozyCornerDaily